Why Would an Annuity Make Sense in 2019?

Annuities barely get a passing thought when the market approaches record returns. Short-term exuberance is addictive and very few people can remove emotion from investment decisions. Well 2019 was a year that paid off for everyone who stuck with it. Trade tensions have eased and the economy seems to keep growing steadily so it may continue for a while. Then again, there’s some real political risk after Thursday night’s news from Iran but that’s an entirely different subject.

Yes, the market was great in 2019 but it was not easy to get there as many people were continually nervous along the way. It seems as though pain is much easier to forget than I used to think because this time last year plenty of people were lamenting the end of a bull market and moderate portfolio losses through 2018.

I remember a year ago I told plenty of people to stick with the market after big losses but I’m not quite as confident this year since many of you have the opportunity to take some nice gains out of play. 2018 wasn’t great and 2019 was. So what is the average of those two years? After all, retirement planning is a long-term proposal so short-term gains or losses are not where you should focus.

I started thinking about this a couple weeks ago and sat down last night to run some numbers. In a post about volatility a few weeks ago I brought up something a lot of people know. It takes a larger gain to make up losses and since 2018 was negative that should decrease the actual yield after a stellar 2019. And of course I wanted to test to see how an index annuity might have affected the outcome. Now, two years is still too short-sighted but it’s a good exercise nonetheless and the difference will no doubt be more pronounced in the long run.

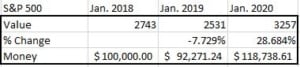

So I took the level of the S&P 500 at the beginning of 2018, 2019 and 2020 to test the value of different portfolio mixes to see what performed best. In 2018 the index was down 7.7% and in 2019 it was back nearly 29%. Starting with a direct investment in the S&P 500 the results are below.

As you can see, after the drop in asset value, rather than being up big the yield was good but a fair bit more muted. The two year effective yield comes to 8.967%. Not a bad average at all but far from knocking it out of the park.

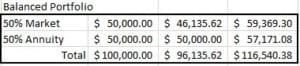

Let’s see how the same thing would look with an index annuity and 50% participation rate…

Instead of risking it in the stock market, had you protected it with an index annuity it would have caused you to come up $4,396 short in portfolio value. But it’s more about what you went through to get the respectable 6.931% effective yield. A year ago most people couldn’t stomach the losses experienced and I don’t know exactly how many stayed in the market. Plenty of others who had annuities were bummed to make little or nothing but no one lost money and there was much less stress involved. Let’s take it one step further and see what a blended portfolio would have done with a 50/50 mix of annuity and stock market.

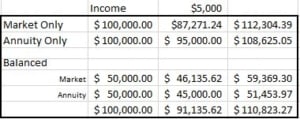

Half of the risk resulted in cutting losses as well and staying in position with a portion of assets to capture more gain, resulting in an improved yield of 7.954%. That’s pretty good considering half the risk. Since you all are in or near retirement then it makes sense to see how withdrawals would affect the outcome. Remember, withdrawals from the market in down years will compound losses so it’s more necessary to protect assets in order to maintain growth potential. Take a look at the final table below where I assume a 5% withdrawal for income in each scenario.

Please allow me to summarize the important points below:

- Taking a withdrawal from market-based assets alone causes a total portfolio drawdown of $6,434, which includes the lost opportunity cost of the growth on the withdrawal. Over several years this will create an exponentially negative affect.

- Using only an annuity gives you a higher starting base for the second year and results in a smaller difference of -$3,679 ending account value. Remember that without a withdrawal the difference between the two was more than $700 greater. This gap will become tighter over several years and will quickly turn positive on the annuity side in times of extended or consistent market turmoil.

- A balanced portfolio again reduces risk but also provides for more growth. The withdrawal was taken only from the annuity side, allowing the market assets time to recover and capture as much gain as possible. This gives a growth advantage over the annuity-only strategy and further reduces the difference between balanced and market-only to just $1,434. Over time this will also swing positive to the side of a balanced portfolio but it happens more quickly and the difference is far more dramatic over periods of high volatility.

What does this tell you? Cutting risk in half more than offsets the limits of only a partial gain. It’s simple and I don’t understand why more people don’t see it that way. Of course the effects are compounded in a scenario where you may be taking systematic withdrawals. Whether you need the income or not it makes sense for anyone who would rather spend retirement on hobbies and family rather than worrying about running out of money.

Stress is bad for your health so why worry about it? Make the decision to blend your portfolio correctly and enjoy a higher standard of living because of it.

Not all annuities achieved double digits in 2019 but some did. If you got every piece of the market or more than you probably don’t need my help or you just got lucky. In reality, emotion caused many to enter or exit at the wrong time and lots of you even paid someone a handsome fee for the pleasure. Get realistic and give me a call if you’d like to see the no risk, no fee approach to growing your money.

Happy New Year!

Bryan

800.438.5121

Last Updated on February 1, 2023 by Bryan Anderson

Brian;

Your illustration looks great, however, I doubt there are many FIA that offer a 50% participation rate for the term of the contract. If you are aware of any please identify those specific fixed indexed annuity’s thank you

John,

Right now the highest is Fidelity and Guaranty at 45% and that comes on all contracts from 7-14 years. I got a call the other day from a marketing firm in regards to a new contract with 50% over ten years but I haven’t called them back to see which company it is.

If we are looking back two years then there were several products that had participation rates as high as 60% on the S&P 500 and I do have active contracts with Equitrust and Lincoln National that have held rates above 50%. These days I am focusing more on other indices that won’t grow as aggressively but have participation rates above 80% so I stand by the 14% but remember it took a phenomenal year to get it.

Over the long run it’s liquidity that gives the FIA an advantage so yield really is a secondary concern. Over historic periods I can lower the par rate to 30% and still produce better results during volatile markets.

Thanks for the question… I figured someone would point that out.