The #1 Rule To Maximize Social Security

Knowing how to maximize social security is always a hot topic. It’s the foundation of many retirement plans. You all paid into it so everyone is entitled to receive something in return after years of contributions. As part of planning for retirement, you need to get an estimate of benefits and compare different strategies for getting the most from the system. It makes retirement easier by lifting the funding burden from your investment portfolio.

In addition to information available from the SSA, there are various forms of planning software and articles that offer general tips for maximizing payments. I recently purchased an advisor subscription to www.maximizemysocialsecurity.com since social security planning has always been a part of what I do. Now I can get the options as technically accurate as possible.

I’m going to show you why going for the highest payment will not necessarily get you the most money. In addition to any projection, you need to also run a break-even analysis to see when the cumulative payments actually add up to more money in your pocket. Articles on how to maximize social security typically recommend delaying as long as possible and standard advice follows a similar line of thinking.

That’s general advice and doesn’t reflect the personal variables that are different for every individual. There are plenty of situations where delaying social security payments goes against your best interests. If you happen to still be working after you are able to claim then it makes sense to delay as you don’t really need the money and the additional income may have adverse tax consequences.

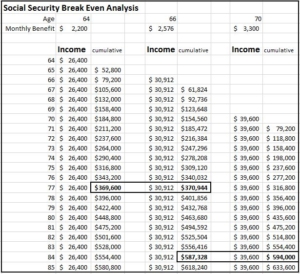

But if you are actually retired and choose to delay payments there’s a cost for doing so since you then need to fund retirement for the interim out of another pocket. To illustrate this issue I’m going to refer to the table below. These are the numbers for Debbie, who I met with recently to answer some questions about her retirement options.

Before Debbie makes any other decisions she needs to firmly commit to a plan for collecting social security payments. She has plenty of other assets so she can afford to pick any option but wants to make sure she does what’s best. As is common, everyone so far has told her to delay taking social security as long as possible to get the highest payment.

As is common, I disagree with anyone who says that and I’ll show you why. Debbie just retired and will turn 64 in a few months so that’s where I started the numbers. Her monthly income needs in retirement are $2200 which is coincidentally the benefit available to her if she claims this year. In the table, I show monthly benefits available if she claims on her 64th, 67th, or 70th birthday. Monthly income is shown beneath each age and the income column for each uses annual income totals. Take a look and I’ll explain below.

Annual income for each year is listed in the first column and the second column shows aggregate payments for each strategy. This is how you need to look at it…

If she waits until age 66 to claim it will cost $52,800 in lost payments in order to receive an additional $4512 per year.

If she waits until age 70 to claim it will cost $158,400 in lost payments to receive an additional $13,200 per year.

If she waited to collect until age 66 she would not actually receive more income until age 77 and beyond. Note the bold box at age 77.

If she waited until 70 she would not actually receive more income in comparison to collecting at age 66 until age 84. Note the bold box at age 84.

Cumulative income numbers to age 85 show a minor cumulative advantage to the delayed collection strategies. If you factor in the out-of-pocket cost for delaying payments she is well ahead by taking the money at age 64.

So, when do you want the money and how much will it cost to wait? For most people, it makes sense to take social security payments as soon as it’s available. My cynical viewpoint is that the SSA knows they pay out less money for the average individual if they can convince everyone to wait. That most advisors suggest a similar strategy reveals a lack of creativity and critical thinking on the subject.

The remaining life expectancy for the average 64-year-old is about 18 years for men and 21 years for women. Half of all people won’t even make it to the point where delaying social security payments becomes worth it. Again, after factoring in the cost of lost payments the comparison is not even close.

Since asset allocation in retirement is dramatically affected by additional income sources I feel that it’s critically important to get this right. Creating a plan based on half information will never be as effective as one that truly considers all angles. Lots of annuity proposals are based on an income gap for someone who is waiting to collect social security. Without waiting the same need doesn’t exist so that type of recommendation is worthless.

If you are waiting then I suggest you reconsider. If someone else advises you otherwise then you need to think hard about his/her motivations for doing so. Feel free to reach out if you’d like to talk about your numbers. Go ahead and call, email, or make an appointment below if you’d like some help to maximize your social security plan for your situation.

Further Readings:

All You Need to Know to Buy an Annuity

Are Fixed Indexed Annuities a Good Investment?

Podcast about how to Maximize Social Security

Last Updated on August 15, 2024 by Bryan Anderson

I read this with great interest because I am turning 64 and have been waiting to file. When I was 62 I did the math and my breakeven at the time was 78. I should do the math again at 64 and see what it would be.

Also, in the 4th sentence below the chart, shouldn’t it read “If she waited till 70” not 77?

Another observation was the breakeven at age 81…taking at 64 instead of 70. $475,200.

Thus is spot on and an excellent resource for folks contemplating when to start.

Thank you for that table illustration!