All You Need to Know to Buy an Annuity

The transaction process that takes you from not owning an annuity to owning an annuity is very simple. Here’s all you need to know.

The transaction process that takes you from not owning an annuity to owning an annuity is very simple. Here’s all you need to know to buy an annuity.

In the past, I’ve worked with several people who delayed a purchase only because of some misconceptions related to the transfer of assets. Rarely does a contract owner have to lift a finger and it’s more automatic than most people think.

First and foremost it’s going to depend on where the money is coming from and the tax status of the funds. It’s all part of the application process and the person selling the annuity should be able to tell you all of this.

All You Need to Know to Buy an Annuity

Ownership

When purchasing an annuity, ownership is an important decision. Most of the time it doesn’t require much thought but once in a while, it is customized to fit in a specific place within a retirement portfolio.

Non-qualified Contracts

Non-qualified contracts can be titled as single, joint, corporate, or trust ownership. It all depends on what you need it to do.

Qualified contracts

Qualified contracts can only be issued in the name of the person who owns the qualified account. A spouse will be the primary beneficiary and take ownership of the account if the original owner passes away, but a spouse can not be the owner when it’s issued.

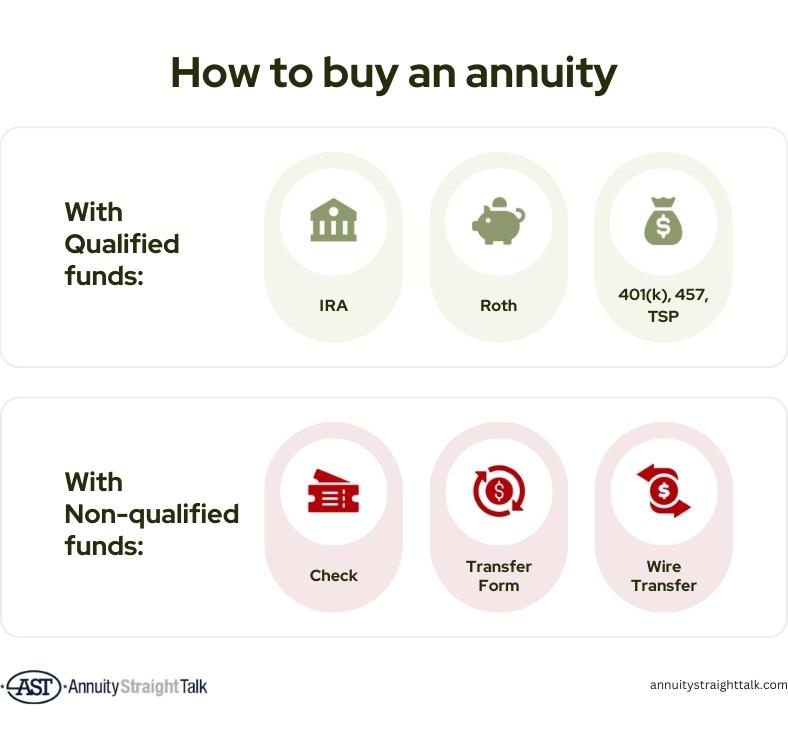

There’s a big difference between qualified and non-qualified assets for obvious reasons. A deeper explanation of each is below along with the process of using each type of funds to buy an annuity.

Who Shouldn’t Buy a Fixed Indexed Annuity

Non-Qualified Funds: After Tax Cash or Otherwise

This is money you’ve already paid taxes on that is currently sitting in a bank or brokerage account. There are three ways the purchase can happen with non-qualified funds.

Write a Check

This is the most familiar option everyone has. When the contract has been approved you can simply write a check to the insurance company for the specific amount of the annuity.

It’s important to write your new contract number in the memo line so it gets to the right place and it doesn’t hurt to include a cover letter with specific instructions. Your agent should be able to handle this and I prefer using UPS to send large sums of money. That way we have tracking info and delivery confirmation.

Fixed Indexed Annuity Withdrawals

Send a Wire Transfer

A lot of people these days don’t have physical checks so a wire transfer is more convenient. A simple request to the insurance company from your agent will get you all the information a bank or brokerage company needs to send the money to the correct account at the insurance company.

If it’s coming from a brokerage account then be prepared for a taxable event if any securities need to be sold first.

Execute Transfer Form

This option mostly applies to brokerage accounts and is good for anyone who wants a hands-off approach. A good number of people are also uncomfortable with a wire transfer. Every application has the option to complete additional transfer paperwork.

During the application, we complete the form with your account details at the current brokerage company. You sign the form and send it to the insurance company. Again I provide UPS labels and envelopes for this.

The insurance company uses the form and works with the brokerage company to have the assets sent to the right place. I will cover more nuances with the transfer form in the qualified funds section below.

If you are buying a new non-qualified annuity with an existing annuity then you will always use option 3, the Transfer Form. If you want to maintain tax deferral then it’s called a 1035 exchange. Just remember that the new annuity has to have the same ownership as the previous annuity. It’s called a ‘like for like’ transfer and not doing it this way will result in a taxable event.

Qualified Funds: IRA, Roth, 401(k), 457, TSP etc…

These mostly cover pre-tax retirement accounts but are also applicable to Roth IRAs. Since these assets are not under your control, it takes the cooperation of the current brokerage company or custodian.

Although most custodians operate the same, several require additional steps so it’s important to know ahead of time so the process is not unnecessarily drawn out. An experienced advisor is more likely to find these things before it delays the transaction. There are a lot of ways this can be done so it’s important to make sure you only have to do it once.

This is a tax-free transfer to another qualified account. Any of the qualified accounts mentioned above will become a Traditional IRA or Roth IRA, no matter what.

Transfer Form

Just like above, this is another form that is part of the application you complete to buy the annuity. Every resigning company is different. Some require original paperwork and signatures, others will accept e-signatures via email and a few companies will accept a photocopy of the original form via fax or email.

Certain states also require consent from a spouse if the contract owner is married. The insurance company handles getting the correct form to the brokerage company so the agent and owner only need to worry about first getting the correct form to the insurance company. Again, experienced agents know what to look for so you don’t have to do it twice.

Additional Requirements

Aside from just the transfer form, some companies like TSP have their own form that needs to be completed as well. Others will not talk to the insurance company and require the account owner to deliver transfer instructions over the phone. Mostly that happens because they want a chance to talk you out of it.

If you don’t know how to look for this ahead of time, the brokerage company will send you a letter and sometimes it goes in snail mail. It could take a while to figure out what you need to do if you’re not working with an advisor who spots this ahead of time.

Sending the Money

I believe that large sums of money should be treated with respect and tracked closely. Wire transfers or overnight shipping seem the most professional to me, but I don’t make the rules.

Uderstanding Index Annuity Fees

Various brokerage companies will use regular mail, overnight, or wire transfers. If you don’t like the potential of losing track of your money then it’s best to call the brokerage company and ask how it will be delivered to the insurance company. You may have to pay extra for a wire transfer or overnight delivery but you can decide whether that’s worthwhile.

Additionally, some brokerage companies will not send the money to an insurance company. Those organizations will only release the money to the account owner. In this case, you’ll get a check first.

The easiest way to handle that is to sign it over to the insurance company, including your contract number, and send it using a reliable overnight shipping service, provided by the agent of course. Some brokerage companies will make the check out to the insurance company in which case all you need to do is send it along.

Buying a new qualified annuity with an existing qualified annuity is no different than transferring money from a brokerage account for the initial purchase. The transaction is tax-free and the tax qualification remains the same in the new annuity.

Check out my Fixed Indexed Annuity Guide.

Knowing What to Expect

Now you know everything you need to buy an annuity. Although this is a lot of information it should not seem confusing. Each person can find what relates to their situation in one or two paragraphs in this post. Knowing what to expect ahead of time will save you from frustration throughout the process. There’s nothing worse than having to do the same work twice because it was screwed up the first time. Working with an experienced professional gives you much better odds of an efficient transaction.

Podcast Episode: All You Need To Know To Buy An Annuity

Further Readings:

Fidelity Annuity Recommendation

Fidelity Investments Annuity Marketing in 2024

Surrendering of Allianz Products