A Better MYGA Option

Well, would you look at that! The Fed just lowered rates but market rates(treasuries and bonds) have already dropped and rose slightly after the announcement, proving you should pay more attention to the market rates when making long-term decisions. It has been happening for the last six weeks or so and everyone keeps saying, “I should do something soon if the Fed is going to start cutting rates.” Since the middle of the summer I’ve watched the top rates drop on all products and that’s well before the Fed made any moves. It has affected some products more than others so I’ll explain how that works.

By far the biggest hit has come to MYGAs (fixed annuities) because there are fewer variables involved in producing the rate. It’s as simple as the spread between the stated rate on the contract and what the insurance company can earn on bonds. Decreases in market rates affect this directly so we’ve seen a downward shift in yield by about 20%. Two months ago people still wanted as close to 6% as possible and now it’s a stretch to get 5% or better. If you want a highly rated insurance company then keep waiting. It ain’t gonna happen right now.

Income contracts have been least affected, whether immediate or deferred. The reason is simple. Everyone has been really excited about short-term contracts, mostly from CDs or MYGAs. I told everyone over the past two years that a one year CD paying more than 5% is good but what happens at the end of that year. People are starting to realize that they can’t renew those CDs at anywhere close to 5% so would have been better off following my recommendation to lock the rate for a longer period of time. Income contracts are built on long-term interest rates, which haven’t been as sensitive and there’s a risk pooling effect with guaranteed income. Mortality credits weigh heavily on income because payouts are based on average life expectancy. Half the people exceed that and half the people don’t so you get an income boost by shifting that risk to the insurance company.

Fixed indexed annuities haven’t shifted nearly as much because there’s another variable involved with yield potential. Remember, indexed annuities let you leverage the fixed rate for more growth potential so the top line comes down more slowly as rates decrease. Contracts I’ve written in the past two years have certain index options that have posted yields in the mid-double digits and new contracts are just as likely to do so when the market is good. With MYGA rates lower, everyone now has a better chance of an indexed annuity outperforming over most terms. I’m going to share an idea that drives this point home.

MYGAs have been a major part of my business over the past few years. It’s an easy contract to understand and returns are guaranteed. But with rates coming down, enthusiasm has cooled a bit. Lots of people wanted the shortest terms possible so we sold plenty of three to five year contracts and we’ll wait and see what is available come renewal time over the next few years. Longer term bets are proving to have been the wise choice but it’s early and we’ve seen year end rate dips in each of the last two years. Like I’ve always said, in ten years we’ll know exactly what we should have done.

Here’s a short-term idea that blends the guarantees of a MYGA and upside potential of the indexed annuity. It’s a five year indexed annuity from Midland National. The key part is that fixed and indexed cap and participation rates are locked for the entire five year term. Currently the fixed rate is 4%, only slightly lower than a good A+ rate with a MYGA and it comes with 10% free withdrawal that not many MYGAs have. With all things considered, this is one of the best places you can park safe money right now

Key highlights are indexes available from NASDAQ and S&P so you can keep it simple or go with one of two available blended indexes that can make big moves when interest rates are volatile. Unlike other contracts with guaranteed index rates that I mentioned in a podcast earlier this year, you can move in and out of each index option and the rates are still guaranteed. You can take the fixed rate when you don’t expect much from the market and take a shot with the indexes when you are optimistic and want a chance at a double digit return. You don’t have to worry about the company reducing growth potential in subsequent years. It only takes a good market and you’ll easily beat a MYGA.

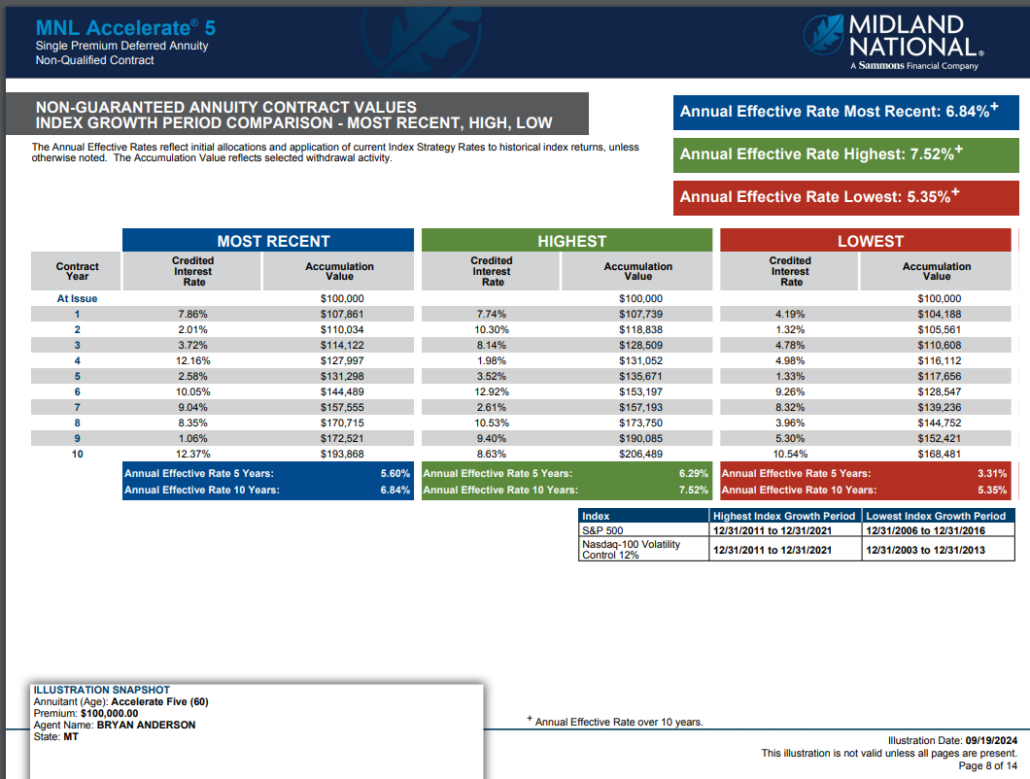

A basic illustration is available below that shows a third of the money in each the NASDAQ, S&P 500, and fixed rate. The past five years show a blended yield of 5.6% and the past ten years is 6.84%. Remember, with 33% of the money only getting the fixed rate of 4%, this would illustrate a lot higher if you wanted to just roll with the indexes. I’ll go over this in more detail during the podcast.

There are those who would still rather have a simple guarantee and that’s fine but this is a solid option that has a very good chance to produce excellent returns with safe money. Rates going up and down is not a bad thing, it only changes where you have an advantage. Give it some thought and make an appointment with me if you’d like to look at it in more detail.

Have a great weekend!

Bryan

Podcast Episode 152: A Better MYGA Option

Download Episode 152: A Better MYGA Option on Apple Podcast

Last Updated on September 20, 2024 by Bryan Anderson