Recover Market Losses with This Annuity

Table of Contents

The stock market reached an all-time high, intraday on January 2, 2022. By the end of the day it had reversed course and it hasn’t been back since. It’s been all over the place since then and it faces a lot of headwinds right now. When it started to drop last year, a lot of people froze and just watched the gains evaporate.

Nearly a year and a half into it, the S&P 500 is still down more than 13%. We are back to the levels of April 2021 so the market has been basically flat for two years after a really bumpy ride.

Waiting for Market Recovery

Dozens of people have told me they are waiting for the market to recover before protecting money. That’s an extremely general investment strategy so I hope anyone using it has deeper analysis to justify it. I don’t think it will happen this year but I could be wrong. Even if it does, what’s the point? The risk has to be worth the potential payoff and there are too many risks present today.

Either way it’s your choice but I do hope you have a backup plan in case it takes a little longer than you expect.

Importance of Timing for Retirement Planning

For anyone who’s ten years or more from retirement, the need to recover market losses matters less because continued contributions will offset volatility and allow for purchase of devalued securities at times.

But most people I’m working with are within a few years of, or are already retired. In this case you have less time to make contributions and/or recover market losses. In addition, creating an income plan while also dealing with these risks makes now an ideal time to start protecting money. It has been studied and proven academically that the five years prior to and first five years of retirement is the riskiest period for consumer investors.

Asset Protection Strategies: Bonds vs Annuities

Bonds are the all-time favorite asset protection strategy for investment managers. It’s been done for so long that millions of people just blindly accept that it will provide protection.

That didn’t work out so well last year when bond values were crushed with rising interest rates.

The annuities I’ve sold haven’t done that well in the past two years but nothing lost value. Fixed annuities are ahead of just about everything else and indexed are as well considering they didn’t lose any value. Annuities are about the only financial asset that didn’t lose money in 2022.

A Different Perspective on Annuities

This week I want to give you another idea, or at least a different perspective on annuities. You don’t have to be in the market to get your money back. Rather than the risk of losing more, you can protect some of it and you will eventually recover market losses but never lose it again.

Higher rates have created more opportunities for investment gains so it’s a good time to switch things up for diversification if nothing else.

You can think of this as an annuity sales pitch if you want, but I feel it’s more like I’m trying to get you to think about it from a different angle.

Benchmarks and Comparisons

Let’s set a few benchmarks first:

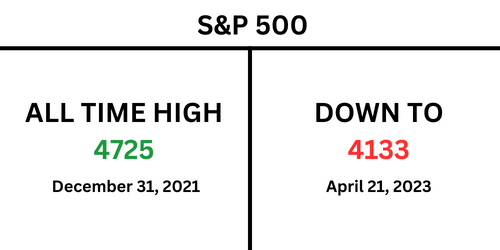

As a percentage of current value, you need 14.5% yield to get back to the value of an all-time high

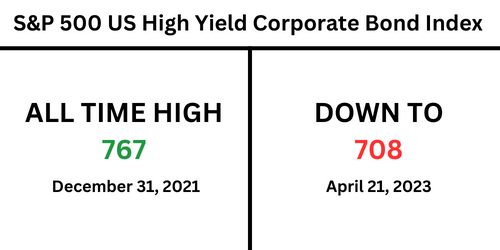

As a percentage of current value, you need 8.3% yield to get back to the value of an all-time high

How To Get Your Gains Back With An Index Annuity

Here’s a quick and easy way to get it back with as little risk as possible.

Like I’ve said for the past year, higher rates have created far more opportunities than you would have had a year ago. I’ve talked a lot about fixed annuities in the past several episodes so now I want to talk about indexed annuities for anyone who wants a little more torque in the product:

Take some money from either the bond side or the market side and buy an indexed annuity.

Right now there are several products with a 10% cap rate on the S&P 500, meaning if the S&P 500 goes up 10% or more then you’ll earn 10%. The best thing about it is that if the market doesn’t go up, you won’t lose money.

You can chase the same thing with market investments but you risk falling back even further.

I feel pretty good about bringing this up now because there are too many economic risks and it seems like going the market route will come with plenty of stress.

Indexed Annuities and Market Recovery

10% yield on an indexed annuity in the first year will get you within spitting distance of the all-time high value, and you’ll continue to climb as time goes by. If you are replacing bonds then you’ll do even better because those haven’t lost as much value. Bonds, however, will recover market losses on their own if the market drops and rates drop with it, as they typically do.

Either way you decide to do it will work better in retirement because annuities are not interest rate sensitive like bonds and they don’t lose money like the stock market can.

Consult an Investment Professional

This is not a recommendation to sell any specific asset just to buy an annuity. Do not do that without consulting an investment professional who can help you determine that it is in your best interests.

I can do it for you or there are a few people I work with closely that can help as well. This is specifically for anyone who is staying in the market to recover market losses but feels nervous about current events and losing money is an unsettling proposition. If you are one of those people you can schedule an appointment and we can have an honest conversation.

Reach out if you have any questions or leave a reply here.

Episode 75: Recover Market Losses with This Annuity

What You’ll Learn from This Episode:

[2:57] Recovering Market Losses with This Annuity

[4:21] The Stock Market Has Been Flat for Two Years: Is It Time to Consider Annuities?

[5:11] Annuity Rates Unaffected by Fed’s Decision to Raise Interest Rates

[6:33] Present-Day Risks: Why Annuities are a Safe Investment Option

[7:15] Understanding the Reverse Dollar Averaging Strategy for Annuities

[10:08] Fixed Annuities Outperform Other Investments in the Past 2 Years

[13:45] How to Make Money and Reduce Risks with Annuities

[14:57] Index Annuities: A Wise Investment Choice with Multiple Benefits

[15:41] Annuities: The Perfect Risk Mitigation Tool for Investors

[19:16] Why Annuities are the Best Option for Distributing Retirement Funds

Key Quotes:

[8:19] “The five years before retirement and the first five years of retirement are the riskiest periods for consumer investors.”

[10:23] “Fixed annuities are by far the best financial assets that you can own.”

[19:19] “If you enter retirement and begin to distribute money, every advantage swings to the annuity side.”

Resources:

Recover Market Losses With This Annuity

Call Bryan Anderson at 800-438-5121 or schedule a call.

Last Updated on May 10, 2024 by Bryan Anderson