The Pros and Cons of Annuities For Retirement

Educated customers understand the pros and cons of annuities before they buy. Watch to see how the right annuity can help you:

- Create protected growth

- Avoid market volatility

- Generate guaranteed income

- All without lifetime locked in commitments.

Understand The Pros and Cons Of Annuities

As with any investment product, there are pros and cons of annuities too. How to decide if the pros outweigh the cons?

To decide if annuities might be right for you, we look at a few key factors. These are crediting rates, income payout rates, the withdrawal restrictions, the corporate credit of the issuer, and the surrender schedule.

Understanding these key elements of annuities allows you to weigh the pros and cons before you buy will help you make an informed decision. Then, when you are ready to buy an annuity, you will have a firm understanding and be able to pick the right annuity for your unique situation.

Please explore the information below, and make sure you understand what you are looking at before making a purchase decision. And be sure to get off on the right foot with the Annuity Guide Report and Video Series.

Pros and Cons of Annuities In General: Pros

The benefits of an annuity are easy to understand. Here are some brief introductions of each of these benefits.

Tax Deferral: Like an IRA, annuity earnings are tax deferred. This makes them more appealing than CDs, money market funds, or other safe investments. Tax Deferred Annuities offer greater compounding of your investment earnings over regular taxable accounts like CD’s or securities investments.

Safety of Capital: Your money is safe in annuities. Insurance companies are required to keep cash reserves to ensure this. Most states also have a guarantee fund up to $100,000 per annuity for additional security.

Liquidity: Your money is accessible. Most contracts have an annual withdrawal clause that will allow you to take 10-15% of the account value each year without incurring any penalty.

Rate of Return: Annuities offer higher rates of return than other safe investments. Currently, annuities are yielding an average of 4% tax deferred in comparison to only 2% taxable with CDs. As our economic markets stabilize, annuity yields should increase accordingly. Annuity rates of return offer more stability in fluctuating markets.

Income stream: Fixed index annuities that provide an income stream have been found to be one of the best retirement income vehicles according to a study done by New York Life and the Wharton Business School. After the first annuity contract year, most annuities can provide monthly income payments for your lifetime. Likewise, immediate annuities provide monthly income payments for your lifetime, but they start immediately.

Pros and Cons of Annuities For Retirement: Cons

The wrong annuity product can have negative effects. It is important to know these cons so you do not purchase the wrong product for you.

Short Term Money: If there is a chance you need all of your money returned to you in the short-term, say one to two years, an annuity is not right for you. It is best to only invest funds you will not need for at least the next five years.

Surrender Schedule: Because annuity contracts have surrender charges for withdrawing money before the contract matures in lieu of up front sales charges, you will be obligated to the terms of the contract. Some surrender schedules can be as long as ten years.

Sales Commissions: As with any purchase, the sales agent will earn a sales commission. An unethical sales agent may not have your best interests at heart and will not show you the right product for your needs.

Liquidity: You may be referring back to the pros section and find liquidity featured there as well. While liquidity can be a pro, it can also be a negative in so much as you realistically knowing how much money you may need to access and when you will need it. Without knowing these answers, liquidity can easily turn into a negative.

This list of the pros and cons of annuities should help you analyze your annuity needs. Use these guidelines to determine what factors are important to you and you will have an easier time selecting the right annuity for you.

The Benefits Annuities Offer

Now that you understand the various pros and cons of annuities, take a moment to understand the types of benefits available to you.

While all annuities are tax deferred, (Unlike CDs and Bonds), there are many other benefits to be considered, and as you review the various benefits available, you can narrow down the options to to types of annuities that make sense for you.

The first major decision point has to do with the term of the contract.

- Lifetime Income

- With Immediate Start Date

- Annuities With Potential Account Appreciation And Surrender Value

- Other Options Without Surrender Value

- With Deferred Start Date

- Options With Potential Account Appreciation And Surrender Value

- Other Options Without Surrender Value

- Fixed Term Income

- Options With Immediate Start Date

- Other Options With Deferred Start Date

- With Immediate Start Date

Understand Annuity Rates

While some types of annuities are pure insurance, with no surrender value, most people refer to have an investment account value paired with their other benefits. When selecting investment type annuities, the main deciding factor is the appreciation rate.

- Fixed Appreciation Rates

- Options with Income Payments, With Invested Principal Compounding Tax Deferred At A Fixed Rate

- Other Options Offer Lump Sum Payout, With Invested Principal Compounding Tax Deferred At A Fixed Rate

- Variable Appreciation Rates

- Options with Upside Potential, With No Downside Risk of Loss

- Other Options With Upside Potential, With Downside Risk of Loss

- Hybrid Options

- Options With Fixed Appreciation Rate With Lifetime Income

- Other Options With Variable Appreciation Rate With Lifetime Income

- Some With No Downside Risk Of Loss

- Others With Downside Risk Of Loss

- Other Options With Lifetime Income With Potential Investment Account Value

If you have analyzed your own situation, you may have a goal statement that clearly guides your decision here. If you’re retired now and need a lifetime income, but want to preserve some flexibility and possible inheritance value, there are just a few options to consider…

Likewise, if you’re still a few years from retirement and need safety, but don’t need to lock in income yet, a fixed term lump sum may make more sense.

Regardless of where you are in your analysis and decision making process, we can help. Start with The Flex Strategy and video series and when you are ready, make an appointment and lets get going!

Want to learn how to use annuities the smart way? Watch the AST Flex Strategy videos.

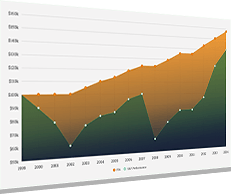

How Does the Right Annuity Secure Your Retirement?

Let’s take a look at how a Fixed Index Annuity performs in different market conditions…

Equity based investments are high risk, highly volatile, and offer no guarantees

Index Annuities form a bulletproof core to a retirement plan that produces great results no matter what happens in the markets

Want to learn how to use annuities the smart way? Watch the AST Flex Strategy videos.

The Flexible Retirement Income Strategy by AST

The Right Annuities safeguard your retirement income from rollercoaster markets

For more than 13 years, Annuity Straight Talk has helped retirement investors avoid volatility, maintain control, and generate guaranteed income – Ready to learn how you can do it too?

We Work With Only The Strongest Carriers:

- Allstate

- Guardian

- John Hancock

- MetLife

- New York Life

- Prudential