Early Retirement Plan Distributions

There are all sorts of restrictions on retirement accounts, especially in regards to , but there’s usually a way to work around each or at least minimize any negative effects. Anyone who wants to retire before 59 ½ needs to know this one and all the ways it can be used. Since withdrawals before that age are subject to an additional 10% tax penalty, it is obviously prudent to avoid this if at all possible. This will stand as a guide for anyone who wants to consider doing this to fund an early retirement.

There is plenty of information about this online but you’ll never find it if you don’t know to look for it. It falls under IRS code 72(t) and you’ll find plenty of the typical websites with information that is helpful. Expert advice is critical as at least one of these sources claims that early withdrawals should be a financial last resort. But if you find someone who can truly look at this from all angles then it can be done effectively. I’m going to say this only for those who are very well capitalized for retirement because you are looking at a longer payout period when starting at a younger age.

Recently a 53 year old couple came to me and we started talking about what would be required for early retirement. They wanted to retire within a year and with a little over 60% of their assets in qualified retirement plans, the 72(t) is probably the best way to get it done. Like many other cases I feel it’s best to work first with the IRAs and leave the non-qualified (after tax) investments alone for long term growth and planning adjustments over time. If you leave the IRAs alone and use non-qualified money to fund the early retirement, long term growth in the IRAs may create adverse tax consequences when RMDs are required. That’s a long way away for these guys but things should still be structured today with that in mind.

Roth conversions can also come into play but in this case that’s something that should be delayed until their early 60s. Deal with one thing at a time in retirement and they have to first figure out how to generate income. Roth conversion and income at the same time will be costly and I’m not sure it’s worthwhile. Plus the rules of the 72(t) are stringent so messing with other distributions at the same time could make things unbelievably complex.

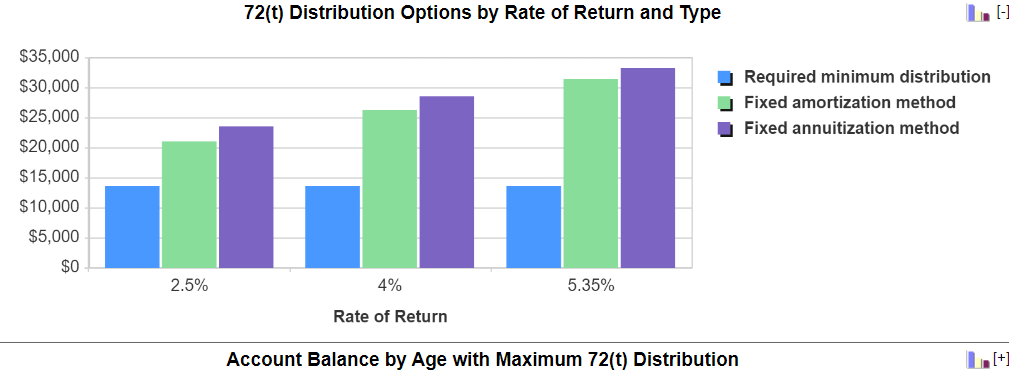

Here’s how it works… the IRS offers three different ways to calculate the amount of penalty free withdrawal. Age of both payees is necessary plus an assumed interest rate that can be no more than 120% of the federal mid term rate at the time it’s set up. Right now that rate is around 5% so the maximum assumed interest rate would be 6%. Using those inputs there are three options listed below.

Amortization Method – This calculates payments based on amortizing the funds over life expectancy of single or joint payees. It results in the highest payments available.

Minimum Distribution Method – This is kind of like calculating withdrawals for RMDs. The IRS issues a table of factors with payouts for each age of single or joint life. This will result in the minimum possible withdrawals.

Annuitization Method – A different set of factors from an IRS table is used to calculate these payments that fall somewhere between the highest and lowest withdrawals for single or joint life.

Any of the above methods can be used to create any type of distributions you want. The result of any method is Substantially Equal Periodic Payments (SEPP) which will dictate the guidelines you need to follow. Don’t mess it up because then you’ll have to pay the 10% penalty after doing all that work. There’s a table below from Bankrate.com that shows the three different methods for calculating a sample $500K case study with an assumed interest rate of 5.35%, and you can see how lower assumed interest rates create slightly lower payments. Click on the image itself to go directly to the calculator on that website.

5.35% happens to be the going rate for a seven year fixed annuity from a highly rated company that would guarantee results. Risk is something you want to stay away from because market volatility is a bad deal when you are stuck with a substantial withdrawal plan. Rules for 72(t) include taking substantially equal periodic payments for five years or until age 59 ½, whichever occurs later. So if you start at age 58 then you have to continue until 63 under the same schedule. No matter what you have to play by the rules at risk of incurring the early withdrawal penalty.

You can find calculators online and play with the numbers but actually putting it into practice requires an expert in products and regulations. This is not for the majority of my audience but is applicable to plenty of people I talk to frequently. If you are considering making this part of an early retirement then get on my calendar and I’ll help you figure it out.

Watch The Podcast Episode: Early Retirement Plan Distributions

Last Updated on October 19, 2023 by Bryan Anderson