Fisher Investments vs. Annuity Straight Talk

I’ve mentioned Fisher Investments several times as part of other topics but haven’t yet gone after it directly. They have a much bigger budget than I do so it’s likely that everyone who finds me also sees the ads from them. I ran into his page for indexed annuities during a marketing call a few weeks ago. I won’t provide a link to it but I do show it on the podcast if you’re really interested in finding it on your own.

What you’ll read on that website won’t really come as a surprise to anyone since Ken Fisher hates annuities, but it should be obvious that there’s a fair bit of bias in what’s written. First of all, they offer to help you evaluate the pros and cons of indexed annuities to help you decide if it’s the right thing to do. How often do you suppose they recommend someone buy an annuity? My guess is that it never happens. So much for evaluating the pros and cons fairly.

Taking it one step further, the page continues to give you three main points to consider, which happen to be a few of the biggest complaints about annuities. Fortunately, I have addressed each of these in my previous work so the combination of what he says and what I say should give you a balanced perspective. I have also linked a couple of newsletters and a podcast that go into more detail about each. Here’s what he says…

Lack of Liquidity: Lack of access to your money is a common issued with most annuities…

This is a myth. Nearly every podcast and newsletter mentions using annuities for retirement income, RMDs or discretionary spending. If you need more liquidity than what is provided in an annuity then you have a bad plan. If you have a short-term need for a large sum of cash, you shouldn’t be using an annuity or market investment. This concern is not relevant to retirement planning.

Fees: Another factor holding back fixed indexed annuities is fees…

Fixed and fixed indexed annuities are spread contracts and have no fees in basic form. You only pay a fee if you want to add a benefit like guaranteed income, death benefit or enhanced growth. All fees are an OPTION and not available with any investment manager. Ken Fisher will charge fees but can’t give you a guarantee.

Newsletter June 26, 2020: All About Annuity Fees

Surrender Fees: If you regret your purchase, you might be locked in by steep charges that last for several years…

The most positive spin on this one is that surrender fees ensure that money never comes out of your pocket. You could pay a front end load on the annuity and get out of surrender fees but the effect would be the same. Fisher used to offer to pay surrender fees for people who wanted to get out of a contract. I’ve met a few people who took him up on the offer. He made them sign a contract, committing to a years-long investment. If they quit early, they’d have to pay him back. That sure sounds like a surrender fee to me!

Newsletter August 15, 2020: Surrender Fees Are Not a Big Deal

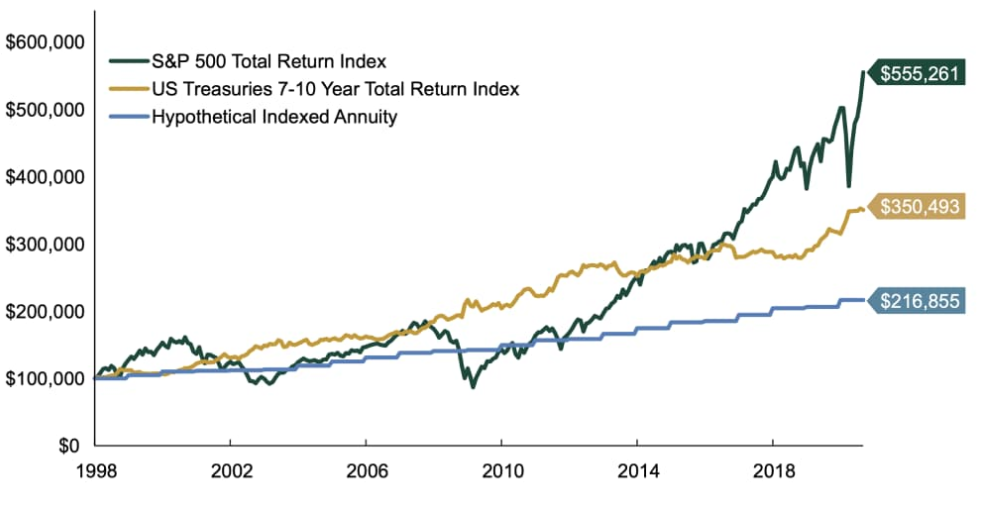

The best is yet to come because Fisher also gave us a chart comparing the growth of three different assets from 1998 to 2020. The chart below shows the S&P 500, US Treasuries, and a hypothetical indexed annuity. This represents cherry picking and bias at its finest and I’m going to explain why.

Clearly, one of the best market periods in history was used. In addition, it was also the tail end of a 40 year bull market in US treasuries. Rates dropped the whole time which continually increased the value of treasuries just like it does bonds. But I’ll give him his numbers and make my point elsewhere. The hypothetical indexed annuity column is what’s most ridiculous. It’s just purely fabricated numbers. Do you have any idea how high cap rates for an indexed annuity would have been in the late 90s? The line he uses totals up to a 3.4% yield over 22 years which is extremely low and not at all indicative of what would have happened.

My main complaint is with the market projection, and I’ll stay away from the fact that the chart ends at the highest historical point. Where are the management fees? He charges for the service, doesn’t he? Well, it was left out of this example but I calculated the effect in the podcast. With anything under $1M in management, Fisher charges about a 1.25% fee annually. That alone would bring the final account value down by nearly $140,000. That’s how real fees affect your pocketbook.

Next, it doesn’t mention anything about retirement income or RMDs. Annuities are for retirement planning and protect a portfolio from a number of additional risks that come when you are retired. None of them are factored in here so the entire page is wildly out of context for anyone of retirement age. If withdrawals are subtracted it makes a completely different picture and illustrates perfectly how an annuity can improve both the experience and the outcome.

Here’s an exact comparison to Fisher Investments:

Why Not an Annuity? Podcast February 26, 2022

Let’s not forget that Fisher is only printing a general look at the S&P 500, not a look at the actual investment accounts the company recommends. Maybe there’s some sort of compliance issue with putting actual performance figures out there. I don’t know, but my guess is that his portfolios probably didn’t beat the S&P 500, otherwise, that’s what would be on the chart. So, Ken Fisher says you don’t need annuities and clearly you don’t need him either.

Take it for what it’s worth but his marketing attempts only tell a part of the story. It’s not annuities or investments, it’s annuities and investments that combine to make a viable retirement plan. If you have a long range investment horizon and don’t need to touch the money then the market is a pretty good place to put your money. If you have a lower appetite for risk and need to actually use your money then an annuity of some type will likely make things better.

The nice thing about all this is that you get to make the call. If you’d like to have a conversation specifically tailored to your situation then get a hold of me.

Further Readings:

The Fixed Indexed Annuity Guide

Fixed Indexed Annuity Withdrawals

Indexed Annuity Crediting Methods

Podcast about Fisher Investments vs. Annuity Straight Talk

What You’ll Learn from This Episode:

[1:43] Fisher Investments vs. Annuity Straight Talk

[4:40] Advertising online, website layouts, and SEOs

[13:37] Is a fixed-index annuity right for you?

[15:13] Bonds: Value increases as rates drop.

[15:28] A favorable yield is based on the reduction of rates over time

[17:28] Index annuities give you tremendous upside potential.

[21:16] Retirement Planning vs. Buy and Hold

Key Quotes:

“This is all about balance, not one or the other.”

“Like anything else, it has to be a fit for you, personality-wise and strategy-wise.”

Resources:

Call Annuity Straight Talk at 800-438-5121 or schedule a call at AnnuityStraightTalk.com

Last Updated on October 1, 2024 by Bryan Anderson

Bryan, you forgot a item that people needs to remember about Fisher.

Fisher will send countless emails and calls even after you refuse to work with them.