Guaranteed Indexed Annuity Rates

Of all the objections that hold people back from buying fixed indexed annuities, this is one of the hardest things for people to understand. Cap and participation rates can change on an annual basis and for good reason, but it just doesn’t sit well with those who distrust insurance companies. This also partially creates the thought that indexed annuities are complicated and that’s not really the case. In fact, looking at this little feature will likely help many people realize that fixed indexed annuities are little more than an enhanced fixed annuity (MYGA).

A couple of years ago I wrote two newsletters that addressed changed rates in indexed annuities. I will update those newsletters and run them as a follow up to this in the coming weeks. We can save the detailed explanation for that. This is not something I’ve ever done on the website but there are indeed a couple of contracts that will guarantee rates for the surrender term. So you never have to worry about adjusting expectations over time because growth potential is reduced. With good companies and contracts it’s not something you need to worry about but this will give you the most assurance from the beginning.

Cap and participation rates on indexed annuities are an important topic to discuss for many reasons. I talk a fair bit about rate shopping with MYGAs and the same thing is relevant here. It’s easier for me than you to keep an eye on pricing for cap and participation rates in the general market. If one company in particular has much higher rates than everyone else then a reasonable person might wonder why. Do they know something that no other insurance company knows? Are they taking greater investment risks than other companies? The first is not likely and the second is not common.

In most cases it’s something I call a teaser rate. The higher cap rate, for instance, will look good on paper but the fine print clearly indicates that it can be adjusted each year. Ignoring the fine print makes for an easy sales pitch and it does get a lot of people to buy. After the first year or two, the rate is likely to adjust down to what’s normal in the market or maybe a bit lower to make up for the added expense in the early years. That’s one good reason why you shouldn’t rate shop indexed annuities. At least one company has stated in marketing materials that the much higher cap rate will revert to market norms after the first year. Stick with good companies and industry averages.

For several years now, a few companies have offered a guaranteed cap rate on the S&P 500. The first contracts that had this would offer a solid adjustable cap rate and one that was just a bit lower that is guaranteed for the whole surrender term. The contracts I had sold in the past came with good renewal rates so the guarantee didn’t seem to be worth much to me. With higher rates it’s a compelling story and also because those who are new to this will appreciate one less moving part.

There are several companies that have this available and I’m going to talk about two specifically. The other ones may be fine but if there’s no material difference between contracts I’m going to stick with companies I know.

Midland National has a five year indexed annuity with guaranteed participation rates on a fixed account and three different index options. Allocate the money and lock in the rates. Let it ride and know you won’t lose anything but still have the potential for some nice returns. Nothing will change so good potential exists for the entire five year term. The indexes available are blended and risk-controlled so it’s hard to do a straight-up analysis of this contract. It’s not a bad thing but I’m going to stick with something simple.

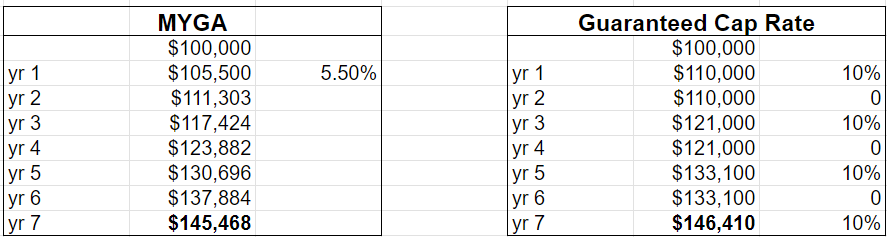

Mass Mutual Ascend, formerly Great American Life, has a five and seven year indexed annuity with a guaranteed cap on the S&P 500. Since it’s the most well-known index we can more easily project decent expectations. On the seven year contract the guaranteed cap rate is 10%, meaning that’s the maximum you can earn no matter how much the market goes up. Looking at the guaranteed rate gives you a solid comparison to MYGAs. Potential will not be reduced so you just have to win a handful of times and you’ll beat the fixed rate.

Currently, top MYGAs are paying about 5.5% for seven years. I built this little table below to compare the Mass Mutual indexed annuity to the MYGA. You can see that you only have to hit the cap four out of seven times in order to beat the accumulation of the fixed rate contract.

The indexed annuity may not always cap out because the market might rise something like 6% in a given year. But it is quite possible to have a positive return in five or six of the years so the potential to beat the fixed annuity is quite real. Like I tell people all the time, fixed indexed annuities are all about deciding whether you want to play the game. If so, you’ve got a solid hand with this.

There is one catch. If you choose to take the guaranteed cap rate then you have to elect it at contract issue and not change it for the entire surrender term. All of the contracts with guaranteed rates have other index options that may yield better in certain years. If you decide to chase another index for one year then you can’t get back into the guaranteed cap rate. You don’t have to put all of the funds in it from the beginning but what you allocate there in year one needs to stay in that option to keep the rate. As an example, you can allocate half of the money to the guaranteed rate and select additional options with the adjustable indexes.

Again, this is just an example of how contracts have been built to be a little more user friendly. I’ve put several people in these options in the past year and everyone likes the assurance of a guaranteed rate along with the simplicity of never having to worry about allocations at each anniversary. If that’s something that appeals to you then get on my calendar and I’ll show you how it all works.

Enjoy your weekend…

Bryan

Podcast Episode: Guaranteed Indexed Annuity Rates

Last Updated on March 15, 2024 by Bryan Anderson

With the annuities and the indexed universal life, do you always still pay 1% fee to the selling agent for the life of however long you hold the policy….. kind of the same as paying someone 1% to manage your investment portfolio? So like in your flex strategy should I expect to pay 1% management fee on that total portfolio no matter who I use ?

Indexed universal life has internal fees related to the cost of insurance. Indexed annuities are completely different and have no additional insurance component. There are no fees for the indexed annuity so there’s nothing missing from the calculations. If you have half the portfolio in the annuity then a 1% management fee would only be charged on the managed asset side, making the effective fee for the whole portfolio .5%

Bryan, I have loved reading about cap and participation rates in these last few newsletters. I like to think of MYGAs just like a bond allocation to my portfolio, guaranteed rate for a preset fixed term. The idea of a guaranteed fixed index annuity is appealing due to potential for excess gains during ‘good’ market years, while maintaining fixed minimum guarantees. In your March 14th newsletter, you show an example chart comparing the MYGA to the Guaranteed Cap Rates. On the Guaranteed side you show several years with ‘0’ growth, I assume these are years with minimal or negative index returns. My confusion is that I assumed there is a minimum guaranteed return, so why is there no growth? I understand returns would be range bound, say 4 at a minimum and 10 as the cap rate. Or do they only give a positive return when the cap rate is met or exceeded?

The table I showed is purely hypothetical intended to simply show a general comparison. In short, I made up the numbers. Indexed annuities are a minimum of zero and maximum of a cap rate or participation rate with no cap. Guaranteed minimum values are a completely different calculation and relate strictly to the surrender value of the contract. It is explained in detail in the podcast below.

https://annuitystraighttalk.com/guaranteed-minimum-annuity-values/