Volatility is probably the biggest concern of most people I meet, but fees may be just as bad for total

performance. Paying fees for any type of investment or manager is palatable for some and not for others. There are several ways a fee can erode investment gains but the highest cost may not be what you think it is. Since I’m a proponent of no fees if at all possible it might help to explain exactly why

that’s the case.I want you to get the highest yield possible. It’s as simple as that. Most people don’t follow the analysis

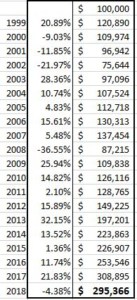

to the point where they can see just how much fees end up costing over time. It’s the concept of lost opportunity cost. If you were able to save or recapture the fee, how would that amount of money grown over time? Compounded annually the total loss is exponentially larger than the annual fee itself.Let’s take a look out how this works. Below are some tables that show a sample investment of $100,000

growing over the past 20 years, ending December 31, 2018. The yields are pulled from the S&P 500 and include dividends. This would closely represent what you could get with a low-cost index fund.

As you can see, the investment nearly triples after all the ups and downs that equates to a little more than 5.5% rate of return. Now the yield would be higher or lower given a different starting and ending time so I don’t want any comments from anyone who wants to argue about performance. I just calculated this off publicly available data.

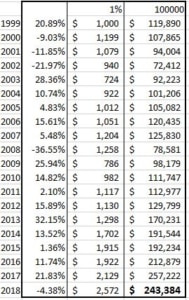

In the next chart I’m going to add a 1% annual fee to the same yields to see how it would affect the total. This is a fairly reasonable combined fee when you add mutual fund or management fees. Some are even much higher so you can decide for yourself whether you are in a better or worse position than this.

The 1% fee may not seem like a lot. It’s just $1000 dollars per year, right? But when you factor in the lost opportunity cost of that extracted amount it decreases the total performance by more than $50,000! A dollar paid in fees is gone and cannot grow with the rest of the money. On $1M portfolio this would amount to over half a million dollars!

What’s interesting is that if you add up all the annual fees the manager would have made $25,943 but the true cost was more than twice that amount. That is lost opportunity cost.

This is a quick exercise to show you why any fee you pay has to return more value than the cost. For instance, if you pay total fees of 1% then the manager or fund should be returning better yields than the market. Otherwise you may as well just open an online brokerage account and buy some cheap index funds.

Along with volatility, fees can really hold you back from achieving suitable investment returns. Reduce fees and you may find a more conservative yield will get you where you want to be.

Have a great weekend!

Bryan

800.438.5121