How to Beat a Guaranteed Income Contract

During Preparation for a meeting this week I was running numbers and comparing options for a couple in California. They had recently been to a dinner seminar to get some answers to retirement questions. Of course the follow-up meeting included an annuity pitch so they decided to do some research online to verify whether they were getting the best deal.

Sound familiar? It should since most of you have done the same thing so I’m writing this to remind everyone of the basic premise behind how I work.

Jack and Beth are both 67 years old, plan to work for three more years and retire at 70 when social security can be maximized. With substantial growth in their portfolio over the past few years they decided now might be a good time to reduce risk and set an income plan in place.

Currently Jack and Beth have roughly $1M in savings. With projected social security payments in three years they need to produce an additional $20K to $30K annually to meet desired spending levels. So the advisor pitched them a product from National Life Group that looks like this:

$500,000 initial premium deferred for three years

14% premium bonus to income account and 7% annual increase

0.9% annual fee for the lifetime income rider

Joint life payments of $32,800 annually starting in year four

During the first meeting Jack mentioned the deal seemed fine to him but he liked the idea of having more control over his assets. So I promised to first verify whether that contract is the best deal available and also run some numbers to see if an alternate strategy would give him more of the benefits he wants.

I took the information from the proposed contract and spent some time looking through the database to find other competitive contracts for that age and deferral period. The National Life contract is at the top end, with a couple options paying a little more and a couple paying a little less. All in all the proposal is right in line with the better options in the market. But would a different strategy improve the results?

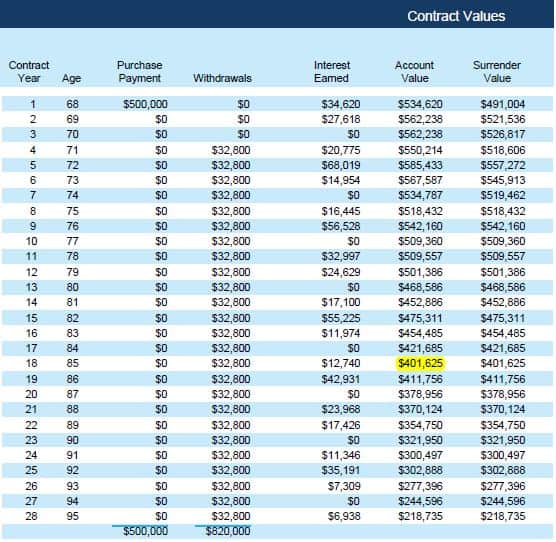

You first need to understand the potential downside of using the guaranteed income contract. I’ve talked about it a lot but never given specific numbers until now. Most importantly, with the above contract the break-even point for Jack and Beth is just past the age of 85. That’s the point where aggregate payments equal the initial investment. It takes until that point in time to realize any profit from the contract. Now that deal would be great for Emma Morano (I had to look up the oldest living person), but the average person is not going to live to the age of 117 and collect payments for more than 47 years.

It’s also important to remember that contracts with bonuses and guaranteed income riders are built with lower growth potential. So in order to start a comparison I first identified a few contracts with more than twice the growth potential of the National Life annuity. By eliminating the income rider it would translate to more than $5000 per year in recaptured costs. The combination of those two enhancements results in performance that offsets withdrawals so Jack and Beth have control over their assets and discretion as to how they are used.

I ran three separate illustrations with contracts built for growth in order to demonstrate that it’s more about how you use the annuity rather than the annuity itself. Each was shown being deferred for three years and then annual withdrawals of $32,800 were shown to match those of the guaranteed income contract. All produced favorable results and I’m going to show you the lowest performing contract below. I do that so no one accuses me of relying only on an overly-optimistic illustration.

As you can see, at the break-even age of 85 there is just over $400,000 remaining in the account. The income contract offered a 14% bonus on the front end but my way gives you an 80% bonus on the back end. The two other contracts projected an account value that was much higher than the initial investment. Because any of them would work I would recommend dividing the purchase between two contracts to spread risk and diversify growth opportunity.

The benefits of doing it this way are explained below in case you guys want a reminder of the advantages of the AST Flex Strategy. If you maximize growth on safe assets you can always take the income you need. Eliminating fees allows you to preserve more capital. A shorter time commitment with more money gives you much more flexibility and opportunity to make changes as the market dictates. The combination of the three puts you squarely in control of your assets through retirement.

Some may say they don’t want to rely on performance of an annuity to produce income. That’s why I added a twist to it that gives this strategy a fundamental advantage over guaranteed income annuities. Traditional use of income annuities separates those assets from your total portfolio. One side is used for income and the other used for growth. The two sides work independently and that gives you less control and decreases total performance.

The biggest disadvantage of using a guaranteed income contract is that the premium is separated from your total portfolio to produce income. But when safe assets offset the risk of market-based assets, income can be drawn from either side depending on market conditions. It produces a coordinating effect for both assets that provides substantially more growth over time. If the growth contract is that much better than the income contract on its own then imagine how much better it can be when used in conjunction with your other assets.

The justification for using an annuity is a different argument altogether and I believe that has been thoroughly covered in previous posts. This happens to illustrate the best way to use an annuity right now. It’s different than what I recommended several years ago but options change over time so I know there will be better opportunities in the future. That’s why I only recommend plans that can change so you can take advantage of my next great idea.

Take a minute to read the July 2020 update of this case here: What It’s Like to Own a Good Annuity

Get the best deal available today but keep your options open so you can pivot if and when a better opportunity arises.

Bryan

800.438.5121

Last Updated on February 1, 2023 by Bryan Anderson

Dear Bryan:

I reviewed the contract illustration you provided in your most recent email. The contract appears to be terrific. Would you kindly provide me with the identity of the insurance carrier and the name of the specific contract. Thank you.

Sure John, I’ll send you some more info in an email. Just a reminder, this was the lowest performing of three contracts I illustrated for the case and I know of a couple others that would work as well. So my recommendation was to split the funds between several contracts with different maturities and growth opportunities.

Brian:

I am a retiring CFP looking to put money into a FIA. Do you work with advisors who can sell for your firm or are you just trying to solicit to new customers?

Sure thing Carl – I am happy to help a fellow professional who wants to do things right. I’ll reach out privately to set up a conversation.

bryan

What if you are already 70 or and in retirement. If one can not wait the 3 years or does not want to wait that length of time. Is it possible to only wait 1 year and then start collecting? Please let me hear your feeling on this and show an illustration if possible.

Thank you. Russ

Yes, you can start taking money any time, whether it be with a guaranteed income contract or free withdrawals from a growth contract. It doesn’t matter if you are already 70, it just might mean a different contract is appropriate. If you’d like an illustration you’ll have to make an appointment.