Misinformation on Annuity.org

For my 100th podcast I’m going back to what got this whole project started nearly 15 years ago. People need straight up education to replace a sales pitch. Back then there was relatively little information available online and now there’s too much. I wasn’t the first to do it but compared to most stuff you’ll see today I was well ahead of the majority. It frustrates me to no end to see the lack of people who are able to explain things simply and accurately.

Most of the annuity information you’ll see online is produced by people who have no stake in your financial outcome. Positive or negative you are likely to at least run into someone who will misrepresent what annuities can do. It may be someone who is hyped to sell an annuity or someone who thinks you should invest elsewhere. A lot of the worst stuff you’ll see comes from organizations, not advisors, and that is what I’m going to talk about today. From the first hundred to the next, I’m going to be honest and do my best to help you learn the most important stuff.

Lately we’ve been working on my website to organize the information and make it easier for people to find the exact answer to their questions. I was told that Annuity.org is a good example of a website that has been put together well. Well it may be organized the right way but my inspection of the content shows that it was certainly not written by an annuity expert. If you were to base a financial decision on that type of information, you may be in for the wrong kind of surprise down the road.

When I first had the idea to start a website we first had to pick a domain. Of course we settled on AnnuityStraightTalk.com but had evaluated several other options. Annuity.org was one that was either available or could be purchased inexpensively 15 years ago. I don’t remember all the details but we were told that .org extensions were mainly reserved for non profit organizations. That didn’t appeal to us because the plan was to make a living doing it. Either way that’s more of a suggestion than a rule but .org does lend some credibility and authority to the content.

It is now a website run by a marketing company who collects names and information to sell annuity leads to other advisors. That’s all part of the business and I guess I don’t mind so long as it has accurate information. That is definitely not the case and I plan to show you several examples. The podcast video is at the bottom of the page where you’ll find more detail on each and where applicable, I linked a previous podcast or newsletter that contains the correct explanation. You don’t need to go through and see them all but any of the individual points below could be what’s holding someone up. Dig into the details that you need to find.

This does apply to fixed indexed annuities and any advisor you work with needs to understand this. Fixed indexed annuities do not have fees unless you buy an additional rider. Commissions are not paid on top of the initial premium. All costs related to selling and placing a contract in-force are part of the internal calculation done by the actuaries at the company. It does not come out of your pocket so this comment is misleading and inaccurate. More information on fees can be found at the newsletter below.

This is just a silly claim. 10-15 years is a long time and I’ve never even heard someone else say that. You can use them right away or wait a couple of years. Some people don’t ever take money out of them but the benefits are derived immediately. Annuities are best suited to be used when you need asset protection or retirement income. Putting a timeline on it eliminates the majority of people that can use an annuity and it’s bad advice. Very few people are setting things up fifteen years in advance.

This is absolutely wrong. It may have been true well in the past when benchmark rates were much higher but this is not how fixed indexed annuities work. The 1% to 3% is the guaranteed growth rate on the minimum guaranteed surrender value. It is not growth on the full principal in the contract. You don’t get a fixed percentage plus the index return. The guarantee you will earn money when the market drops only accrues to the surrender value, not the account value. A claim like this needs a much deeper explanation but fortunately for you guys I’ve already done it.

Guaranteed Minimum Annuity Values

Wrong. Mortality and expense fees only apply to variable annuities. This is simply incorrect with no need for much embellishment. I wrote an entire guide about variable annuities and that would be a good start for anyone who wants to dig deeper into the subject. It doesn’t apply to fixed indexed annuities so it shouldn’t be on the page.

A Simple Guide to Variable Annuities

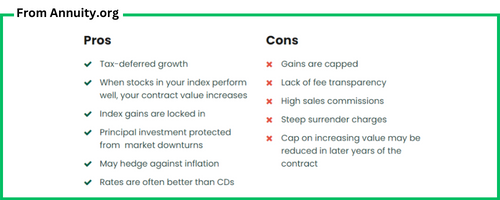

The Pros are fine but the Cons are weak. Not all gains are capped and fee transparency is vague and mostly doesn’t apply like I mentioned above. High commissions are not material to the contract itself and ‘steep surrender charges’ is meant to create an emotional response. All in all this is ok but I prefer objective explanations. My page on this has been up for a long time and I think it’s better.

Fixed Indexed Annuity Pros and Cons

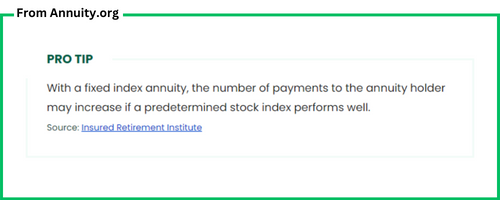

This is a pro tip, huh? Funny because it relates to an incredibly niche income product that might have indexed payments. It does not relate fixed indexed annuities. Since this relates to a benefit some people would want then you have to make sure it is fully explained. I haven’t even seen one of these products in a long time and have only talked to one person who was interested in it. Forget this little pro tip even exists.

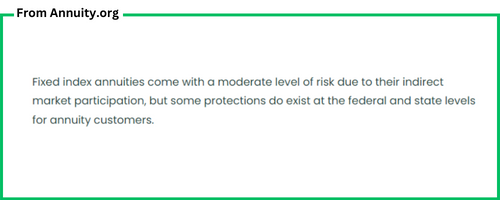

Fixed indexed annuities do not come with any more risk than a plain fixed annuity. There is no federal protection for annuities and the state funds are not something you should rely upon. I’ve covered the topic of insurance company failure extensively and if the point is raised it requires a far greater explanation.

What Happens if an Insurance Company Fails?

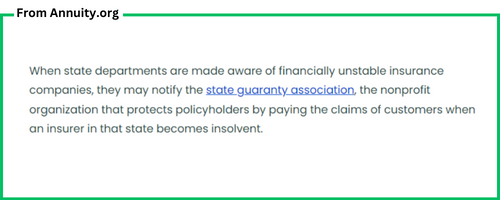

State Guaranty funds do not operate in a clearly defined way. It’s not as simple as calling the state association and paying out a claim. It takes years of rehabilitation and liquidation of an insurance company before the state ever becomes involved. Never buy an annuity based on the existence of a state guaranty association. Yes, it’s there, but you should focus on the strength of the company above all else.

Here we go again with the non-existent fees. Commissions certainly affect the motivation of some agents but it’s not a disadvantage of the contract itself. Some gains are capped but many are not. Like everything else, this is a narrowly focused comment that needs much more explanation.

I’ll give them the whole idea of a balanced portfolio. That is fine but fixed indexed annuities do not have elements of a variable annuity. There is no similarity and it’s kind of lazy to explain them that way. There is a specific way that fixed indexed annuities work and the details need to be laid out in a clear format. It’s impossible to get a good education when all you have is misinformation.

Indexed Annuity Explained on One Page

Fixed indexed annuities are just as safe as fixed annuities. Both are built the same way. The guaranteed minimum return relates to the surrender value and not the protections on the account value.

Artificial Intelligence in Financial Services

There are several other slight examples but it’s not worth my time to pick it apart more. This all needs to be pointed out because everyone deserves an accurate portrayal of all financial products. On Annuity.org I get the impression that much of this was done with AI. Various informational inputs can be given to a program to create a document that will repeat the main points. It can be seen a lot throughout the entire page with inaccurate information repeated in exactly the same way.

Be careful where you get your information because it may not always be true. Search engines are looking for keywords and format, not expertise and accuracy. Unfortunately, you don’t get answers to your questions, you get the answers they want you to see. I’ll keep producing original content and hopefully you can see the difference. It’s quite important for making good financial decisions.

Bryan

Watch the full episode

Last Updated on February 6, 2024 by Bryan Anderson

I’m thinking of buying a North American fixed index annuity with a guaranteed lifetime payout for my wife and me. I’m putting 4.4 million after tax dollars to buy this annuity. The annuity will pay 310k/yr for lifetime 310k/12 or $25,830/ month. The guaranteed income rider has been figured in to this payment schedule. I’m retired and 77 y/o, my wife is 62. What do you think? Thank you.

If you are already retired and your goal is to provide income for your wife, you should go for it. North American is solid but there’s a chance you can get a higher payout elsewhere. Let me know if you need some help.