Part II: Adjustable Index Annuity Rates

Last week I tried to explain to everyone how rate adjustments work within an index annuity contract. It’s an objective matter that offers little insight as to the structure but there is plenty of room allowed for the inquisitive mind to make a rational decision. Even still, some feel as though the matter of interest rate adjustments relies simply on the mood of an insurance executive when renewal time comes. I don’t blame anyone for feeling that way because my suspicions suggested the same years ago and only continued evidence to the contrary allowed me to change my opinion.

Yes, there are contract options that guarantee rates will never drop. There aren’t many but these options exist for those who want added assurance and don’t mind limited options. Anyone who doesn’t like adjustable rates has an option, although the guaranteed rates don’t always have as much potential. After writing this initially in 2021 I predicted that there would be more of this and now, a few years later, it turns out I was right.

On the adjustable side, there are many factors at play that I alluded to last week and I received some sharp feedback that questioned my analysis. Since I don’t believe anyone else goes to this depth to explain contracts, I would expect the benefit of the doubt for my efforts. My objective has always been to give everyone as much information as possible so that each person can take control of their financial future for the right reasons. If you don’t like what I say then take someone else’s word and run with that.

The truth is that rates change every year for fundamental reasons, not based on someone’s mood. The price of bond funds changes daily, up or down. The price of stocks and dividends paid change constantly as well. Sure, you can sell a stock or bond at the current price at the moment you decide the terms don’t work. If so, what else would you buy? Maybe a bond that yields less or a stock at a higher price that creates a lower effective dividend?

There are many ways to poke holes in my argument based on bond yields and stock dividends but I’ll just come right back and talk about the volatility associated with either. The biggest reason I’m right is because I’m talking about something that definitely doesn’t fluctuate in value. It only goes up. Although several advisors will take a different approach, this solution is for those people who want justification for taking the path of true stability for some assets.

Several years ago, one person decided not to buy a few years ago because he thought rates would drop without notice and the insurance company would work the game against him. I have sold several similar contracts since then so I looked up the illustration from the initial proposal, wondering how much rates have changed since then.

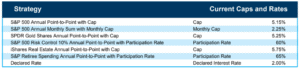

Here are the index options and associated rates from the Great American (MassMutual Ascend) contract I proposed in September 2017.

When I saw that I realized that those were pretty good rates and that anyone now would be crazy to pass those up. Then I realized that there were a few other people who did in fact buy the same recommendation at that time. I looked up one contract and found something that many might consider to be unbelievable…

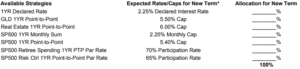

The following numbers are from a contract that was issued in October 2017 so the timeline, given IRA transfer times, lines up perfectly with the illustrated rates from above. This is from the 2020 renewal letter so these rates are what is available entering the fourth contract year.

Here is objective proof that rates can in fact rise as well as drop, so long as certain economic conditions are met. It is an adjustable rate that works in your favor just as easily as it can work against you. It’s the same contract in both cases, one illustrated just two weeks before the other was issued. My goal for each person was to find a solid growth contract and I think I did a pretty good job.

Whether a contract increases rates depends partly on how the bond portfolio that backs the annuity is structured. Midland National is another company I use a lot and insiders have told me that they take a long-term pricing approach that gives them confidence that rates will remain steady throughout the surrender term. Before I sell anything from a particular company I have to do my best to figure out whether I can rely on information like that. It took the leap with Midland almost six years ago and here’s a good example of rates remaining steady until now.

This contract is almost five years old and this first shot is from the contract data page at the front of the contract. It was issued with a fixed rate of 2.7% and S&P 500 cap rate of 5.15%. Going into the fifth contract year, those rates haven’t moved a bit and it still holds the same growth potential. That’s just a good snapshot of the general rates in this contract. There are lots of index options in this one and it’s one of the better performing contracts I’ve ever sold. It turns out that what the Midland internals told me seems to be true.

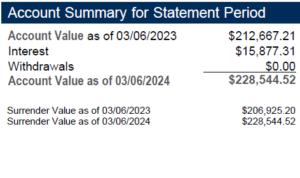

And finally I’m going back to MassMutual Ascend because I had one very well performing contract recently become surrender free. I knew the indexes were up approaching the anniversary so I crossed my fingers on behalf of the contract owner and she topped off a solid seven years with a very nice return. Starting value last year was $212,667.21 and the final interest credit was $15,877.31 for a tidy yield of 7.47%. You won’t be able to convince her that she got a bad deal.

So you have the choice. Get guaranteed rates or go with more options and adjustable rates. It seems that in either situation you’ll maintain growth potential throughout and we just looked at evidence supporting the claim. Some rates rise or fall, some stay steady and indexed annuities either way will hold good potential for all years you’re in it. If the three examples above don’t have you convinced then another asset is probably more suitable for you. In the end it’s always your choice and I just want to make sure you have all the information necessary to make good decisions.

Let me know what you think… comment below or respond to the email if you have anything to add.

Bryan

Further readings

Fixed Indexed Annuity Withdrawals

How Much Do Fixed Annuities Pay?

Podcast Episode: More Proof Index Annuity Rate Adjustments Aren’t A Bad Thing

Last Updated on March 29, 2024 by Bryan Anderson