The True Cost of Volatility

Gains in the stock market are great but losses create stress. It’s high times on Wall Street right now and any painful experiences of the past are distant memories for most people. Even so, volatility is the top concern for a majority of people who are exploring the possibility of using annuities in retirement.

Most people think about volatility in terms of losing money. There’s more to it than that. Losing money is temporary but there’s a long term affect that can cause more damage and reduce the probability of success in retirement. Volatility also reduces long term yield so the more you have the less your assets grow over time.

It may seem obvious but have you ever really looked at the numbers? I mean, everyone is likely familiar with the idea that a 50% loss in one year requires a 100% gain in the next year to break even. As bad as that loss would be, the worst part is that bad luck followed by great fortune only gets you back to the starting point so you would have gone nowhere over a two year period.

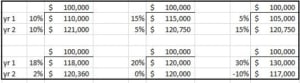

I’m going to share with you a basic exercise to drive this point home. I’ve been doing this with people since the beginning of my career and it’s a simple way to show you how more volatility reduces the final yield. Refer to the table below to see several examples of a two-year time period with alternating returns. Add the yield from each year together and divide by two. Every example averages 10%.

Curiously, as more variability is introduced to the yields, the result drags down the ending account value. The highest value comes from a steady 10% each year and the lowest value comes from 30% growth followed by a 10% loss. The explanation lies in the difference between arithmetic and geometric average. Basically, one provides an average of the yields and the other gives the actual yield on investment.

Managing risk properly leads to greater yields over time by reducing volatility to improve performance. It matters even more in retirement because systematic withdrawals compound losses and limit gains. If you want to visit the archives you can look at something I wrote in 2011 about Reverse Dollar Cost Averaging. The game changes when you retire and start living off your assets. Your strategy needs to change so you can play the new game effectively.

In my last post I showed you how the opportunity cost of management fees drag down performance. Volatility makes it even worse. I had promised to offer the solution but felt it necessary to include this as well since the eroding effects of volatility can cause even more damage.

Next time I’ll put down some hard numbers that show clearly the benefits of reducing fees and managing risk properly. It’s all about making the most out of what you have. If anyone feels like jumping the gun then give me a call and I’ll show you how it works before sending it to anyone else.

Until next time…

Bryan

800.438.5121

Make an appointment

Further readings:

The Fixed Indexed Annuity Guide

Are Fixed Indexed Annuities a Good Investment?

How Much Do Fixed Annuities Pay?

Last Updated on May 10, 2024 by Bryan Anderson