Which Annuity Would You Choose?

I ran into a standard example last week when Sharon scheduled an appointment and asked for me to review an annuity proposal she had received. Without naming names I’ll say that the proposal came from a large national firm that advertises aggressively for index annuity sales. I know well how the company works and have had issues with several of the advertised claims over the years.

This time it was no different. The proposed contract would produce exactly the amount of income Sharon needs in five years and she was also told she could expect healthy account growth giving her additional access to the money, long term income increases and a substantial remainder after 20 years or more. It’s the last three things in there that are misleading. It’s fine to purchase guaranteed income products but doing so under the wrong assumptions will set you up for disappointment. If one of the overstated benefits is meant to provide something necessary then not getting it could cause financial hardship. That’s why we have to be careful with recommendations in this business.

This is a different way of looking at the same issue I’ve been writing about for a long time. Many other advisors are jumping on board with this strategy now but I can document my research on it all the way back to 2005. Yes, I’m not afraid to claim I was the first person doing it this way.

Let’s talk about this case. Sharon was planning to put about 40%, or $500,000 of her assets into a contract that when combined with social security would fully meet her income needs when she retires at age 68. The illustration shows guaranteed income of $35,000 annually in five years. That hit her goal perfectly so she is seriously considering buying the annuity.

Forget the specific companies or contracts, let’s just look at the likelihood of the additional benefits promoted by the agent. As everyone should know, additional withdrawals in excess of guaranteed income payments will reduce future guaranteed income payments. Substantial account growth is needed for additional withdrawals, income increases or to leave a remainder at the end.

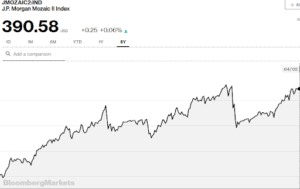

In order to determine whether that’s possible we need to look at the growth potential in the contract. It happens to be one of my old favorites. The advisor suggested the JP Morgan Mozaic II index as the best way to make all the good things happen in the contract. The only option within the contract requires a three year crediting term and the agent produced numbers that show the index has averaged more than 8% historically. Why don’t we look at the past three years to see if it’s a realistic claim?

Over the past three years, the index grew from 358.86 to 390.58 which equals an index gain of 31.72 points, returning 8.84% for the term. The contract offers 130% participation on the index along with an annual spread of 1.5%. And we can’t forget about the guaranteed income fee of 1.1% annually. Let’s add it all up to see what we have.

130% participation brings the yield to 11.5%

But there’s a 1.5% spread each year so 11.5% minus 4.5%(3×1.5%)

Final yield of 7% in three years

Also you need to subtract the fee for the income rider which is 1.1% annually

You would have guaranteed lifetime income but your account will barely grow and once income withdrawals start the account will drain quickly. My educated guess is that the account value will go to zero sometime around the 20th contract year. Sharon would still have guaranteed income but that’s with no additional withdrawals, no income increases and no remainder account value when it’s all over.

Sharon doesn’t want to pay a fee but she is beginning to come to terms with it because the product hits her future needs perfectly. So I was tasked with finding options to see if it could work the same way without paying a fee. Again, without mentioning product or contract let’s see how a different growth opportunity works to solve her problem.

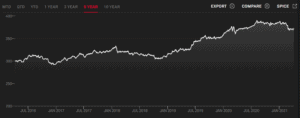

This is not the first time I’ve mentioned the S&P Multi Asset Risk Control index. It is offered with one and two year reset options so let’s see how it did in the past two years? That will get as close as we can get for comparison.

Over the past two years the index grew from 325.17 to 372.96 creating an index gain of 47.79 points for a total yield of 14.7%. Participation rates also apply but there is no spread or income rider fee.

14.70% return multiplied by 105% participation rate brings the yield up to 15.43%

No fees to dilute the account value or spreads to drag down performance

Income rider is not necessary because you can have free withdrawals to take the income you need

Pure growth and efficient control of account

Contrasting account values: JP Morgan Mozaic II grows to less than $520K in three years while the S&P MARC 5 produces more than $560K in two years.

If you are going to skip a guaranteed income rider because you want no fees, more control and more flexibility with your assets, there are several things to consider. Most importantly, how much is left down the road and will the account hold up to substantial withdrawals? Here’s how that looks with similar withdrawals:

3% average growth leaves remainder of about $250K in 20 years

4% average growth leaves a remainder of over $380K in 20 years

5% average growth never invades the principal

This is all when the other account would have likely gone to zero

Easy question: Which option provides more flexibility?

A lot can be accomplished when you avoid fees but it’s not for everyone. The payouts for a guaranteed income contract is higher in this case because it’s a single life payment. For anyone wanting a joint life payment the alternative without the guaranteed income is going to look even more compelling. Just imagine how much more money would be left in the account if the income payments aren’t as high.

There is also a faulty assumption that in either case you have to keep the annuity for the rest of your life. If you have fees, low growth and high income payments there might not be much money left if you want to do something different but you still can. Knowing that a change in planning may be needed the alternative without fees produces more growth and makes additional opportunities more likely if interest rates rise or plans change over time.

Curiously enough, the quoted income contract was not even the highest paying contract on the market. I found one that produces a few thousand more annually in five years. That means Sharon could spend less money for the same benefit. She has a decision to make but at least I’ve got some good news for her.

So let me know. Which annuity would you choose?

Bryan

800.438.5121

Last Updated on February 1, 2023 by Bryan Anderson

If you put [REDACTED] in an Immediate Annuity life time pay out jointly, what is the return. Is only the interest taxable being you are getting principle an interest paid to you?

Vito – that depends on the age of the payees and a few other factors. I’ll send you an email and let you know what I need to produce a quote.

Bryan am in agreement with you. Its one thing to give income guarantee. yet it does not matter what illustration the principle is almost alway gone by 85. When you strip a policy down of fees and caps you often can meet clients income needs yet maintain flexibility and leave something for heirs. This is why we love what we do. There is no perfect plan no one size fits all. Everyone needs and expectation are diffrent and require a square peg square whole mentality. Many ways to achieve needs and goals. Appreciate you sharing your insight and knowledge and exsperince.